Problems at Blackpearl Group?

Blackpearl Group was recently listed on the NZX. I’ll be honest with you - I only started reading about this because I wanted to understand what on earth Blackpearl does. So let’s answer that question first, and work from there.

What the hell does Blackpearl do?

Blackpearl offers SaaS products. NewOldStamp is an email signature automater, whilst BlackPearlMail is an email automation tool which also offers email signatures, email stats, banner advertising and so on. That’s it.

The NewOldStamp Acquisition

NewOldStamp was acquired for NZ$4,858,691 last year. The deal comprised of $600,000 in cash and $999,729 in stock issued at $1.25 per share, and then, basically, two swaps of i) 719,659 in shares at a price of $1.25 and NZ$900,000 of shares at the average market price twelve months after purchase and then 623,510 in shares (at $1.25) and $780,000 in shares at the average market price twenty four months after purchase.

Did you get all that? The complications of it may make it seem like Adobe acquiring Figma, but be assured, reader, this is a humble, er, email signature business. Ok then. Obviously, a bunch more shares will be issued to satisfy the deal, but this seems to be par for the course with Blackpearl - the company also issued warrants to chairman Tim Crown’s entity, Crown BP Holdings LLC, in return for a loan of ~NZ$2.1M. The warrants should dilute shareholders by an additional 7.19%.

So far we have a company that has two businesses - both mail-related, a lot of dilution ahead, and a stock price that has declined +50% since listing (currently trades for 50c per share, listed for $1.25).

Why write this up? It’s clear this listing was for regulatory reasons and the intent was not to raise capital (unlike My Food Bag - trading at 40c per share as of writing) - perhaps the Blackpearl folk, most of whom are wholesale investors who should know what they’re getting themselves into (Owen Glen, as well as billionaire car dealer Larry van Tuyl). Yet Blackpearl is a listed company and is subject to the same scrutiny as any other public company, and the CEO has been on something of a public relations tour promoting his company. Fair game.

Is Blackpearl a “serial acquirer”?

The stated intention of Blackpearl is to acquire other small and medium-sized businesses. I wrote a little bit about serial acquirers in my last newsletter - I own Eurofins, which is a serial acquirer, and LVMH, which is basically a serial acquirer on a really massive scale. These companies make money and explicitly buy profit generating companies (LVMH-aquired Tiffany’s generated $541M in net profit for 2019, when it was a separate company). As far as I can tell, NewOldStamp has never been particularly profitable, which leads me to my next point.

The numbers are a dumpster fire.

Let’s start with NewOldStamp, which has consistently lost money for both 6 months ended ‘22 and ‘21. One has to wonder - why buy a company which is losing money when your company is also losing money?

Blackpearl Mail, the company’s “core” business, has also consistently lost money

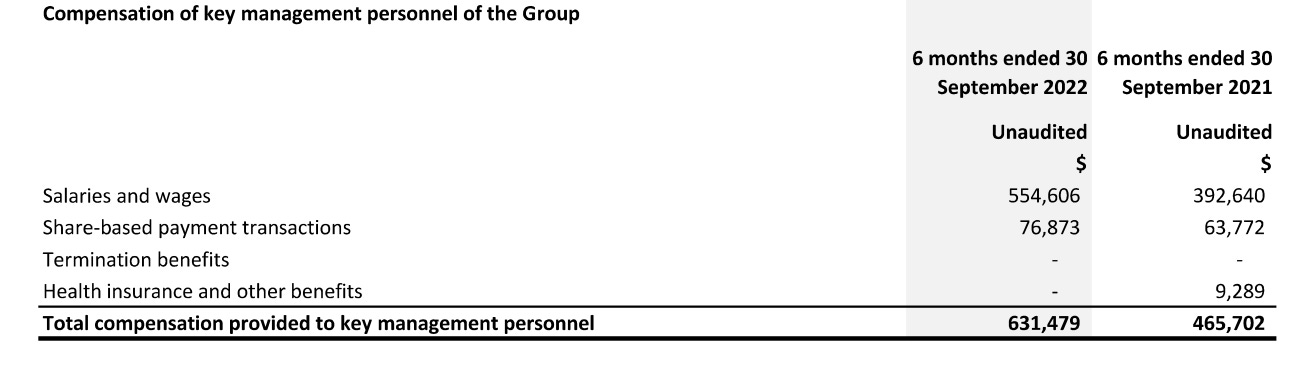

While the “core company” has grown subscriptions well YoY, personnel expenses and operating expenses are bonkers - $1.56M at 6 months ended ‘22. Aprox $172k of ‘21 figures are from government grants, as noted here. Management is not shy about compensating itself, either:

I am not the best with numbers - this is not sarcasm, I actually have to write things down and work through them very slowly, like a simpelton. However, even I wonder what a company is doing paying out “key management” more than the company’s gross revenue. Is there a golden goose I did not know about?

It doesn’t take a genius to guess that Blackpearl’s pro-forma statements that include NewOldStamp are even more of a dumpster fire - net cash flows for the year ended 31 March ‘22 are negative $3.7M.

What is Blackpearl Group’s strategy?

This is the question any investor should be asking, and what I suggest management of Blackpearl should be asking themselves. Blackpearl listed at the arbitrary price of $1.25 per share, which assumed a market capitalisation north of $40M (currently its market cap sits at just $17M). It loses money. Even through the very liberal arthemitic of EBITDA and adjusted EBITDA, it loses money. It acquired a company that loses money. Are there profitable acquisitions on the horizon? How much will the SMB market be affected by the recessionary economics of internet spending right now, and how will that impact upon Blackpearl’s top line? Jerry Maguire said it best: show me the money!